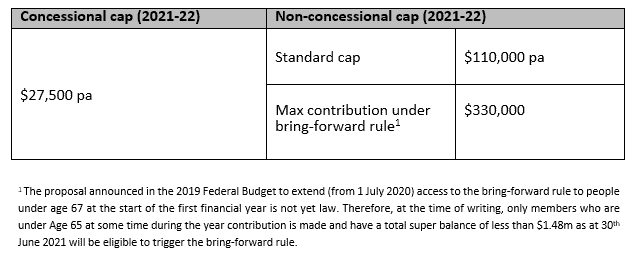

From July 1st 2021 the concessional and non-concessional contribution caps are set to increase due to indexation as follows:

So what does this mean for planning right now?

For a start, indexation of the concessional contributions cap (from $25,000 to $27,500) automatically flows through to an increased non-concessional cap ($100,000 will become $110,000) and the general transfer balance cap will also increase (from $1.6m to $1.7m) from 1 July 2021.

This is where things get a little complex, but we can also now populate the table of bring forward thresholds and amounts for 2021/22. It’s complex because it depends on both the increasing general transfer balance cap and the increasing non-concessional contributions cap.

The $1.59m threshold above is:

The general transfer balance cap ($1.7m)

Less

1 x the annual non-concessional contributions cap ($110,000)

Importantly, the same table applies to everyone. While the personal transfer balance cap will be different for different individuals from 1 July 2021, this table of contribution thresholds depends on the general transfer balance cap ($1.7m) regardless of the individual’s personal cap.

There are a number of important flow on impacts for clients.

Timing of large non-concessional contributions is important

Those considering large non-concessional contributions will need to think carefully about whether they do that in 2020/21 or 2021/22.

Consider a 60-year-old client with a $1m total superannuation balance at 30 June 2020 who has not previously used the bring forward rules but is about to do so.

Contributing $300,000 now locks in the 2020/21 non-concessional cap of $100,000 for all three years (2020/21, 2021/22 and 2022/23) even though the cap will actually increase next year. All other things being equal, it may be preferrable to contribute $100,000 now and $330,000 in July 2021.

What about those with slightly more super – say, hovering around the $1.4m mark?

They have a delicate balance between:

- Contributing the full $300,000 now while they are still below the key threshold for this year ($1.4m at 30 June 2020), vs

- Contributing only $100,000 now, increasing the total superannuation balance and possibly impacting their ability to maximise their bring forward in 2021/22.

For example, if this client’s total super balance was instead $1.35m at 30 June 2020, a $300,000 contribution would clearly be possible in 2020/21.

Contributing $100,000 in 2020/21 instead, however, might mean their balance at 30 June 2021 scrapes over one of the new thresholds ($1.48m). Their non-concessional contributions would be limited to only $220,000 in 2021/22 (a bring forward period of two years rather than three).

All that said, even this outcome is not such a bad thing. While it might not be as much as they had hoped ($100,000 in 2020/21 and $330,000 in 2021/22), the total contributed for the three years up to 30 June 2023 would be $320,000 ($100,000 in 2020/21 plus $220,000 in 2021/22). That’s still better than putting the full $300,000 in now.

Watching unexpected impacts on the bring forward rules

We all like to think that bring forward periods are carefully considered and happen exactly when the client meant to use these rules to maximise their non-concessional contributions.

In fact, remember that they are triggered automatically whenever the annual non-concessional cap is exceeded. The contributor has no choice about the period of the bring forward. If someone with a total super balance of $1m at 30 June 2020 has even 1 cent more than $100,000 counted for their non-concessional contribution cap in 2020/21, they will automatically lock in a three year period up until 30 June 2023 and their non-concessional contributions over that time will be limited to $300,000.

Traps for the unwary are small contribution amounts that have been forgotten about which cause the person to exceed the cap even though they thought they had only contributed $100,000. For example:

- personal contributions to an industry fund to maintain insurance cover

- personal contributions for which a tax deduction has been denied

- spouse contributions

- SMSF expenses paid personally that weren’t reimbursed, and

- excess concessional contributions where no action was taken on the excess notice and so the contributions remained in the fund (remember these only count towards the non-concessional contributions cap if they are not refunded)

Double deduction strategies for SMSF clients

A strategy sometimes employed by those who need a large tax deduction in one year but not the next is the “double deduction” strategy. A common example for someone who is (say) no longer receiving employer contributions is:

- contributions up to the concessional contributions cap are made any time during the year (say 2020/21);

- an additional contribution is made in June 2021 but not allocated to the member until July 2021; and

- a personal tax deduction is claimed for two years’ worth of contributions in a single year (because both contributions were made in the same year) but the contributions count towards the relevant cap in different years, avoiding any nasty excesses.

So what’s different now? If that strategy is being adopted for 2020/21, don’t forget that the second contribution in June 2021 can be $27,500. This is because it’s being tested against the 2021/22 concessional contributions cap – and by then, the cap will be $27,500.

Conclusion

An increase in the contribution caps can only be a good thing for clients targeting higher super balances to help optimise their financial position. Whilst it gets a little complex, the strategy opportunities at a client by client are significant.

Next steps

To find out more about how any of these measures may be of assistance in your individual circumstances, please contact Gordon Thoms or David Conte at Calibre Private Wealth Advisers on ph. (03) 9824 2777 or email us here.

This advice may not be suitable to you because it contains general advice that has not been tailored to your personal circumstances. Please seek personal financial and tax/or legal advice prior to acting on this information. Before acquiring a financial product a person should obtain a Product Disclosure Statement (PDS) relating to that product and consider the contents of the PDS before making a decision about whether to acquire the product. The material contained in this document is based on information received in good faith from sources within the market, and on our understanding of legislation and Government press releases at the date of publication, which are believed to be reliable and accurate. Opinions constitute our judgment at the time of issue and are subject to change. Neither, the Licensee or any of the Oreana Group of companies, nor their employees or directors give any warranty of accuracy, nor accept any responsibility for errors or omissions in this document. Gordon Thoms and David Conte of Calibre Private Wealth Advisers are Authorised Representatives of Oreana Financial Services Limited ABN 91 607 515 122, an Australian Financial Services Licensee, Registered office at Level 7, 484 St Kilda Road, Melbourne, VIC 3004. This site is designed for Australian residents only. Nothing on this website is an offer or a solicitation of an offer to acquire any products or services, by any person or entity outside of Australia.