The start of a new calendar year tends to draw out the forecasters. People are naturally curious to know about what the future might hold. But the list of uncertainties appears to be particularly long as we head into 2022 – starting with the path of the pandemic, but also encompassing inflation, central bank policy, climate change and geopolitics.

Events in early 2020 humbled even the most careful forecaster. After a solid start to the year in global share markets, prices went into dramatic reverse in March as the reality of the pandemic hit. Major indices fell by 30% or more in the space of weeks.

Assiduously compiled projections and forecasts made only weeks before were quickly shredded. Assumptions for global growth, inflation, investment, unemployment and dozens of economic and market variables were rapidly unwound.

As it turned out, the world economy quickly recovered, although with the exception of the US, not to the levels prevailing before COVID. share markets, after their savage decline, rebounded in equally dramatic fashion to reach record highs.

Two years later, and with the pandemic still raging, who can blame forecasters for seeking to hedge their bets about 2022? After all, hopes have been raised repeatedly, and then dashed again, as new variants emerged. For central banks seeking to withdraw emergency stimulus, there are questions also about where to strike a balance between heading off resurgent inflation and keeping the recovery alive.

For investors faced with this storm of uncertainty, there is little alternative but to stick to the basic principles of diversification and discipline – staying focused on their goals, maintaining a reserve of cash and resisting the urge to respond to information that is already reflected in market prices.

But that doesn’t mean one shouldn’t seek to stay informed, regularly reviewing the risks to the outlook and maintaining flexibility where needed. As always, this should be done with the guidance of a professional adviser who knows you, your family and your aspirations, understands what you can live with and builds you a portfolio to maximise the chances of you reaching your goals.

In the meantime, here is a brief summary of the state of play as we enter the New Year.

The Big Picture

For all the doom and gloom around, world economic output continues to grow. According to the Centre for Economics and Business Research (CEBR), a UK-based think tank, global GDP will rise 4% this year to surpass $US100 trillion for the first time.

Separately, the International Monetary Fund in October projected a more robust 4.9% global growth rate in 2022, although this forecast was made before the appearance of the Omicron variant and the disruptions resulting from it.

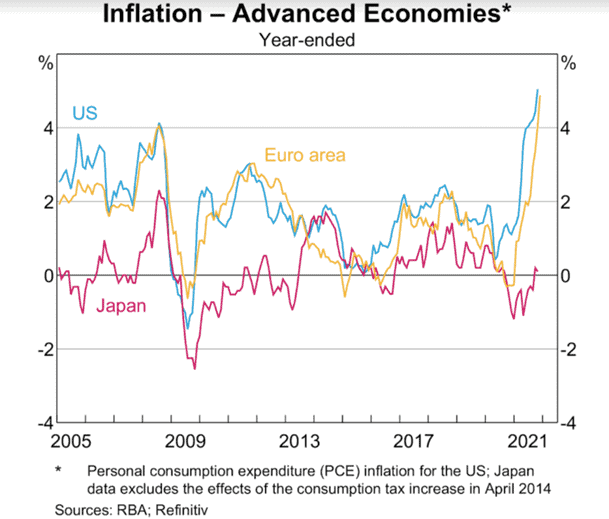

The wild card, according to most forecasters, is the path of resurgent inflation. This is most pronounced in the US, where the headline CPI soared by 6.8% year-on-year in November, its largest annual gain since 1982. In the UK, inflation jumped to 5.1% in the same month, its highest rate in more than 10 years.

“The important issue for the 2020s is how the world economies cope with inflation,” says Douglas McWilliams, deputy chairman of CEBR. “We hope that a relatively modest adjustment to the tiller will bring the non-transitory elements under control. If not, then the world will need to brace itself for a recession in 2023 or 2024.”

Already, we are seeing policymakers start that adjustment process. In December, the Bank of England became the first major central bank to raise interest rates since the pandemic began, voting 8-1 to lift the bank rate from 0.1% to 0.25%.

In the US, the Federal Reserve, which has already begun reducing its purchases of government bonds, has flagged three quarter percentage point increases in its benchmark overnight rate in 2022, with the first move expected by March.

The Case for Hope

As always with any overview of the economic and political outlook, however, it is worth recalling that risks are not tilted in one direction only. And, for this reason, a wise investor will maintain some allocation to growth assets.

In a recent article for Foreign Affairs (a leading magazine for in-depth analysis and debate of foreign policy, geopolitics and global affairs), economist Charles Kenny – a senior fellow at the non-partisan, Washington-based Centre for Global Development – provided five reasons to be optimistic about the outlook in 2022.

The first of these is increasing rates of vaccination in the developing world, with as many as one billion doses scheduled to arrive in Africa by March.

The second cause for optimism is the accelerating transition in the world’s energy sources, with the largest increase in global electricity generation from renewables expected in the coming year.

A third reason for hope is democratic India, which as it celebrates the 75th anniversary of its independence this year, is on track to take over from China as the world’s most populous nation.

“After years of hearing that the future belongs to a rising, authoritarian China (a narrative much peddled by the country’s rulers themselves), it will be a much-needed lift for the democracies to see one of their own rising in importance,” Kenny says.

The fourth reason echoes the CEBR view – that after the COVID-led contraction, advanced economies will post 4%+ growth this year. As well, many countries are getting much better at handling economic shocks.

A final reason to stay positive is the progress the world is making in slowing the loss of biodiversity, with advances in modern agriculture improving the productivity of land use and reducing deforestation.

Conclusion

That the world faces major uncertainties in 2022 goes without saying. The threat of inflation, questions over the pace of withdrawal of stimulus, and, most of all, the path of the pandemic make forecasting an even more hazardous occupation than usual.

For investors, it may offer comfort to know that financial markets price these risks constantly as new information comes to hand.

But we also know that risks don’t all go in one direction. We know that the global economy has significantly recovered from the initial shock of the pandemic, that our understanding of the virus is increasing, that vaccinations are increasing globally, and that economic innovation continues in areas such as energy and land use.

Innovation and improved productivity hold out the hope of more sustainable ways of growing and preserving wealth. Investors can share in that by participating in global markets and maintaining a balanced outlook.

None of us know what the future holds. But we can prepare ourselves for whatever happens by focusing on what we can control and maintaining a realistic sense of hope.

Next steps

If you have any questions/thoughts in relation to this article or would like more information, please contact Gordon Thoms or David Conte at Calibre Private Wealth Advisers on ph. (03) 9824 2777 or email us here.

The information contained in this article is of a general nature only and may not take into account your particular objectives, financial situation or needs. Accordingly, the information should not be used, relied upon, or treated as a substitute for personal financial advice. While all care has been taken in the preparation of this article, no warranty is given in respect of the information provided and accordingly, neither Calibre Private Wealth Advisers, its employees or agents shall be liable for any loss (howsoever arising) with respect to decisions or actions taken as a result of you acting upon such information.

This advice may not be suitable to you because it contains general advice that has not been tailored to your personal circumstances. Please seek personal financial and tax/or legal advice prior to acting on this information. Before acquiring a financial product a person should obtain a Product Disclosure Statement (PDS) relating to that product and consider the contents of the PDS before making a decision about whether to acquire the product. The material contained in this document is based on information received in good faith from sources within the market, and on our understanding of legislation and Government press releases at the date of publication, which are believed to be reliable and accurate. Opinions constitute our judgment at the time of issue and are subject to change. Neither, the Licensee or any of the Oreana Group of companies, nor their employees or directors give any warranty of accuracy, nor accept any responsibility for errors or omissions in this document. Gordon Thoms and David Conte of Calibre Private Wealth Advisers are Authorised Representatives of Oreana Financial Services Limited ABN 91 607 515 122, an Australian Financial Services Licensee, Registered office at Level 7, 484 St Kilda Road, Melbourne, VIC 3004. This site is designed for Australian residents only. Nothing on this website is an offer or a solicitation of an offer to acquire any products or services, by any person or entity outside of Australia.